")

picture_in_the_city

You could say I miss Chrysler. That’s saying something considering all the problems the carmaker is now facing as part of Stellantis NV (NYSE:STLA) had over the decades, to the point where it the auto industry’s favorite punch line. In its current form, with a P/E ratio lower than almost any other stock I know, it’s still not cheap enough for me. That’s because of a number of quantitative and technical factors that I describe below.

As with any dividend stock I look at, I look at STLA through the lens of my YARP™ (Yield At a Reasonable Price) methodology. To recap, YARP is a process I developed over the past decade with my then-teenage son, who was one of several summer interns we had at the investment advisory business I ran and sold in 2020.

That was a year before STLA was formed through a merger of Fiat Chrysler Automobiles and the PSA Group. While that combination resulted in the world’s fifth-largest automaker at the time, it has been a difficult road since then.

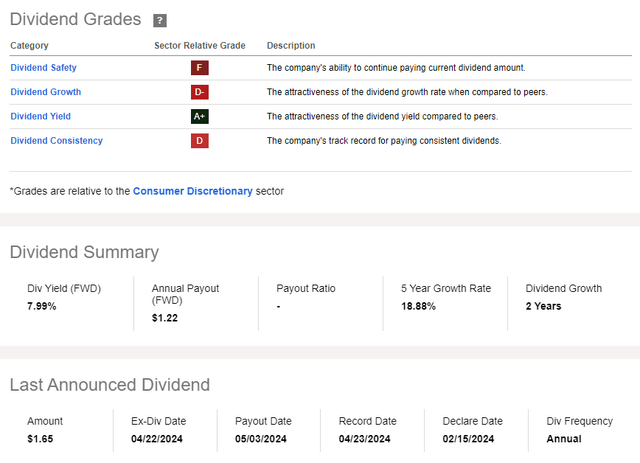

Dividend at risk? YES, according to SA Quant Grades

YARP looks at a stock’s dividend history, and one of my concerns with STLA is that the dividend “could be history” if the company doesn’t get its act together soon. Seeking Alpha’s quantitative dividend ratings have been fairly accurate over time, with more than 60% of F-rated stocks having their dividends cut, suspended, or outright eliminated. Guess what rating is here? F.

As a European company, STLA does not pay a quarterly dividend like most US stocks. It is an annual payout. I am not a deep fundamental analyst, but more of a technician and quant. But I wonder if there will even be an annual dividend payment here in 2025.

I’m looking for Alpha

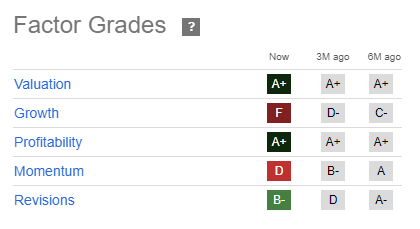

Is STLA a profitable stock? Absolutely not!

My YARP methodology would kick STLA out the door, so to speak. Before I consider a stock for my YARP portfolio, it must pass several non-technical tests. Since I am not a fundamental analyst, I need to be sure that the dividends and price appreciation I am targeting will not suddenly be disrupted by factors that a fundamental analyst would immediately recognize.

In Seeking Alpha’s quantitative terminology, that means strong profitability ratings, typically at least B, but preferably in the A range. STLA does indeed pass that test. However, this is the automotive sector, and a strong position within that group requires a very generous rating scale.

I’m looking for Alpha

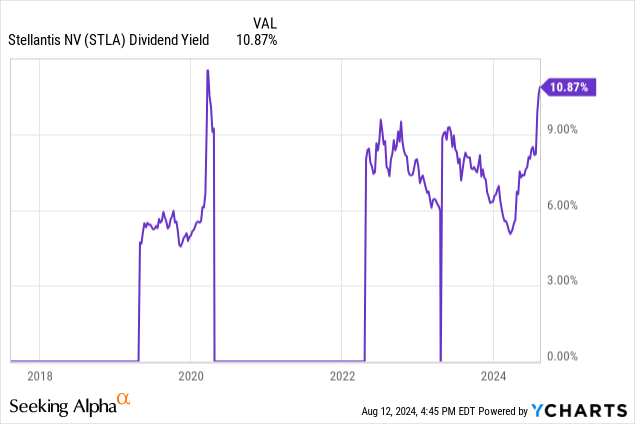

My YARP approach also requires a 7-year dividend history, as a key to the YARP factor is evaluating where the dividend yield currently sits relative to that 7-year history. The chart below shows that STLA’s history before and since the Chrysler acquisition has produced a very uneven dividend yield pattern. And even if that weren’t the case, my 20-year YARP backtest history for hundreds of stocks shows that when the yield is at or near a 7-year high, as shown below, it’s “very high risk/very high reward.”

It also doesn’t hurt that STLA is rated A+ on valuation. But as a self-proclaimed “strict evaluator,” I look at this dividend situation and despite the cash position and other fundamental signs of strength, this is not a YARP stock for me.

I’m all about avoiding risk first and foremost, so I won’t jump right into it here unless it’s a small “flyer” position. Below I’ll cover the technical/price pattern potential for STLA, since a YARP/dividend-driven case is off the table, so to speak.

Morgan Stanley’s Monday note on STLA sums up the sentiment around this stock quite well:

After a “disappointing” first half of the year, Stellantis is facing a “difficult situation” given potentially weaker volumes in the second half of the year as well as price and production pressures due to high inventories in North America. As a result, the investment company now expects an adjusted operating profit margin of around 10% for the full year 2024, compared to over 11% previously. Morgan Stanley also cut its revenue forecasts by 10% in 2024 and 5% in 2025 due to expected lower revenues for the company and pricing headwinds across the industry. According to the release, the company also cut its earnings per share forecasts by 23% and 8% in 2024 and 2025, respectively, due to expected lower revenue generation and the company’s lower production.

According to Morgan Stanley, there is a potential increase in sales volumes if Stellantis significantly reduces dealer inventories, but this could come at the expense of higher incentives for dealers. “We believe the inventory situation will pose challenges for Stellantis in 2024, but will not change the equity position. We expect the merger to continue to generate cost synergies and note that management has demonstrated its ability to execute to date,” Morgan Stanley said.

Morgan Stanley lowered its price target for Stellantis from $28.40 to $20.75 and maintained its overweight rating.

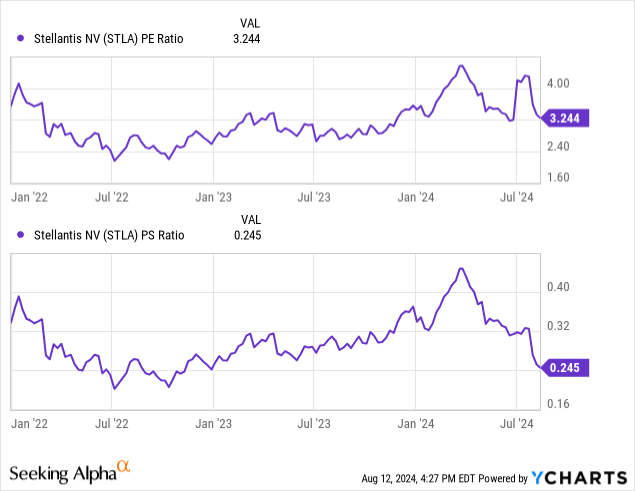

For me, low profit and sales ratios do not mean “cheap enough”

That’s because a microscopic P/E based on trailing earnings is nothing new here. The share price is back to 2017 levels and only half of its March 2024 peak. So this is not an ignored name. Not with a market cap of $44 billion.

Technique: How deep can you go?

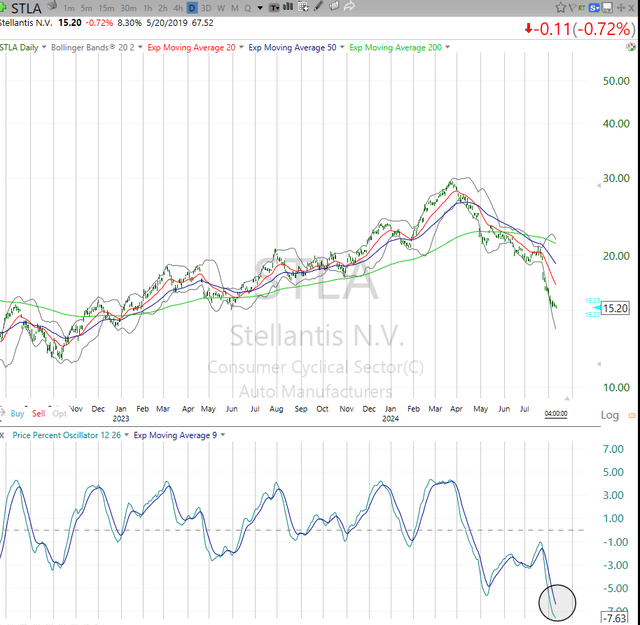

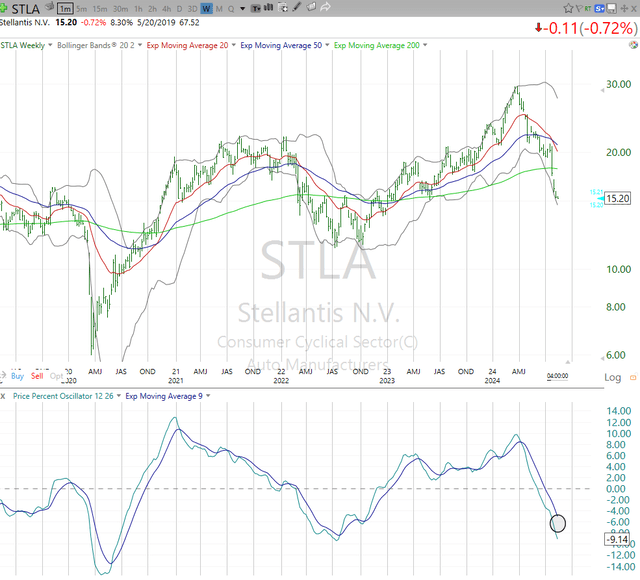

I present a daily chart and a weekly chart just below. STLA has arguably fallen to what we chart geeks call “long-term price support,” as the stock bottomed here about 14 months ago. But the circled section below on the momentum indicator I rely on, Price Percent Oscillator, PPO, essentially says, “I might start thinking about slowing my decline, looking for a price bottom here, and then maybe, just maybe, I’ll be a good buy in this general area.”

TC2000 (SungardenInvestment.com)

TC2000 (SungardenInvestment.com)

Conclusion: I stay in the slow lane with this car giant

In other words, as I said before about a stock with a dividend yield at at least a multi-year high, this is high risk. And potentially high reward. But personally, I can’t get past the first part of that thought.

I didn’t miss the fact that Stellantis’ ticker symbol is the same as Tesla’s (TSLA), just with two letters swapped. I’m not a huge fan of either. I’m recommending STLA as a sell, knowing that it could be one of those deeply contrarian turnaround stories at some point. But that’s too far-fetched for my stock-picking methodology.