")

Various photographs

Semiconductor stocks as a group have been hit hard in recent weeks. Even top performers like NVIDIA (NVDA) lost much of their value before hitting lows in early August, but the group has since regained value. then. Whether this is a recovery or the beginning of a new, sustained rally remains to be seen.

In this article we take a new look at Applied materials (NASDAQ:AMAT), which announced its third quarter results on 15th. Last time I covered AMAT, I concluded that second-quarter earnings were not good enough. I have similar conviction about third-quarter earnings. Let’s take a closer look.

Hard resistance from above

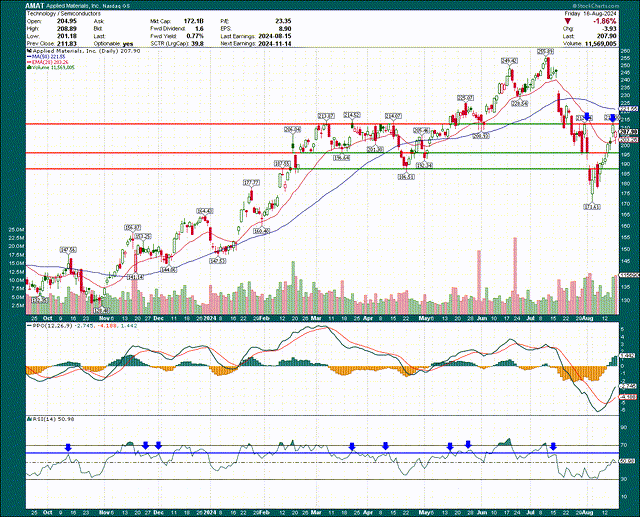

We start with the chart as always and I think that in the case of AMAT we have a very difficult overhead that the bulls will have to overcome, if they are even able to do so.

Stock charts

On the daily chart, we can see very clearly that the level is at $214. That was the high of March (twice) and also April. Also, after breaking through it, it was support in June and then again in July. Now that it has been broken through, it has been resistance that has been broken twice in the last few weeks. The point is that it is really difficult to be bullish on AMAT below that level because it looks to me like $214 is a wall at the moment.

The RSI is also struggling to break above 60, which I have marked with a blue line at the bottom. This is a level that is difficult to reach during sideways or bearish periods, and AMAT has not seen a reading above it since early July. The RSI suggests that the bears are in control for the time being.

On a relative strength basis, it is even worse.

Stock charts

AMAT has massively underperformed its peers (top pack) over the past few months. And in the bottom pack, we can see that the semifinalists as a group have underperformed the S&P 500 since June. While much of that has been offset by the run-up we’ve seen, AMAT is actually a terrible performer in a weak pack.

Finally, the seasonality for AMAT is very unfavorable in the next six weeks.

I’m looking for Alpha

September is the worst month for AMAT this year, so comparing that to relative strength and the price chart itself, I think the chances of $214 holding are extremely high. If you’re a buyer of AMAT, I think that means you can wait and see and potentially get a much better price.

Q3 was okay, but not good enough to buy

I mentioned that I reacted to the third quarter results in much the same way as I did to the second quarter results. The results were OK, but not enough to support the valuation.

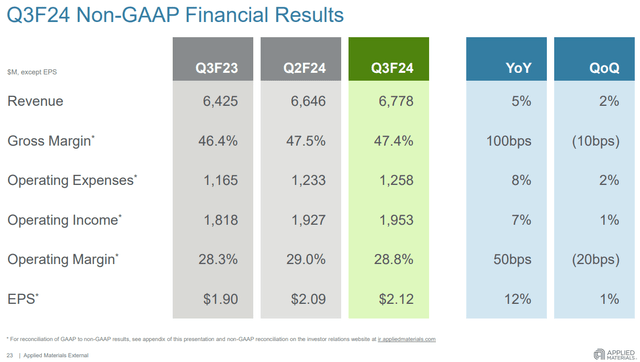

Adjusted earnings per share were $2.12, 10 cents above estimates. Revenue rose 5.4% year over year to $6.78 billion, beating expectations by $110 million. That’s all fine, and fourth-quarter guidance was essentially in line. Again, fine, but not spectacular.

Management has said that the race for AI leadership is driving demand for the company’s products and services, and I don’t doubt it. But at the same time, when you look at the growth rates of other names in the semiconductor space, AMAT’s growth rates are more like those of a consumer goods stock and should be valued as such.

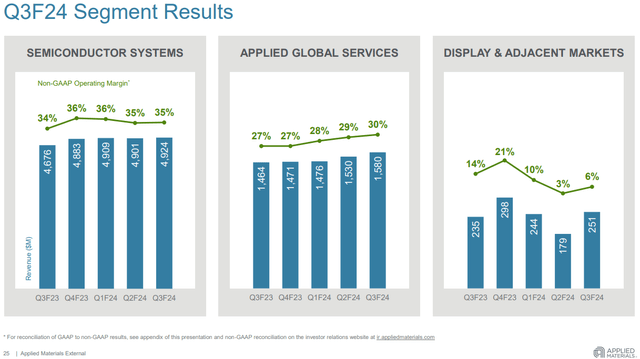

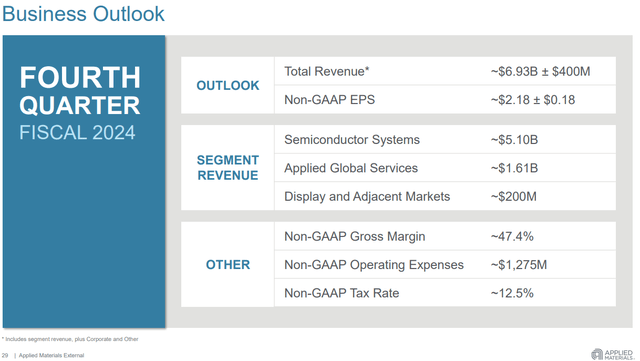

The core semiconductor systems segment generated $4.924 billion, up $248 million from the third quarter of last year. The forecast for the fourth quarter was $2.18 earnings per share, three cents above analyst estimates. Revenue is expected to be in the range of $6.93 billion.

This is what the estimates for the last quarter of the year look like.

I’m looking for Alpha

Revenue growth is fairly muted this year but should pick up in 2025/2026. Importantly, analysts expect earnings per share to outperform revenue for the foreseeable future. That will require strong margins and/or strong buyback activity to achieve that. Let’s take a closer look at the third quarter results and see if AMAT is on track to achieve that.

Investor presentation

We see that operating profit grew faster than revenue and that’s because gross margins increased 100 basis points year over year to 47.4% of revenue. Part of that was offset by higher expenses, which increased 8% and ate up half of that gross margin gain. This is a key variable going forward.

Investor presentation

Operating margins in the company’s largest segment have been flat for several quarters, so it’s difficult to make a difference here. AGS has sustained higher margins, but its contribution to revenue is relatively small, so it doesn’t make much of a difference when consolidating results. DAM is negligible in terms of revenue and margins. The point is that it’s likely to continue like this going forward, unless AMAT has a wild card up its sleeve to drive meaningful margin expansion in semiconductor systems.

Investor presentation

The fourth quarter guidance assumes flat gross margins compared to the third quarter, but potentially slightly higher operating margins as cost growth is expected to be less than revenue growth. This assumes the company reaches $6.93 billion. Note, however, that the revenue guidance is +/- $400 million, which is a large Number. We’ll see, but what I’m saying is that it doesn’t look like margins are going to significantly increase profits any time soon.

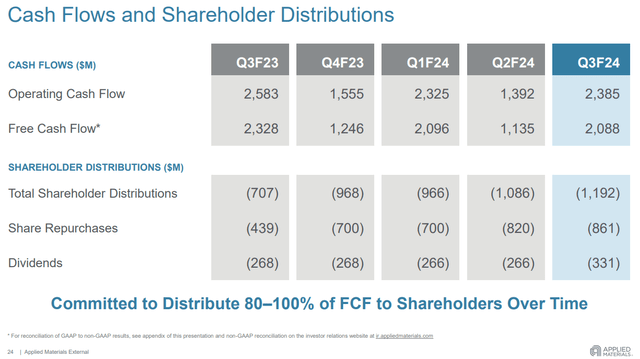

AMAT does a good job of allocating cash and we can see the company spending $700-$800 million per quarter on buybacks quite reliably.

Investor presentation

This represents an annual tailwind of around 2% to earnings per share as the free float is reduced. As long as this continues, earnings per share growth should outpace revenue growth. FCF was well above total distributions, so there are no sustainability concerns here.

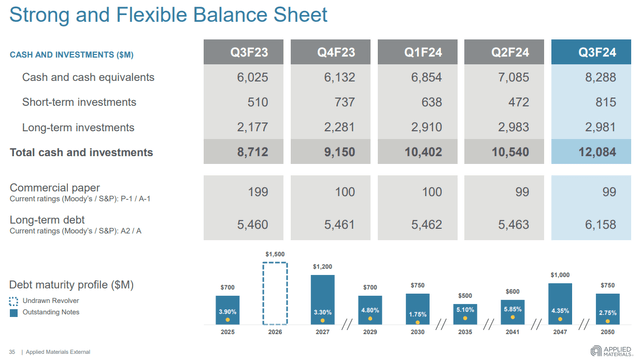

This is especially true given AMAT’s balance sheet, which appears quite robust.

Investor presentation

The company has $12 billion in cash and equivalents, net debt is about -$5.8 billion. There are absolutely no balance sheet concerns here and AMAT has the flexibility to invest in growth, acquisitions, buybacks or whatever else it wants.

AMAT is being put up for sale following third-quarter results

The final piece of the puzzle here is valuation, and to me it is the nail in the coffin for AMAT’s bull case. To be clear, AMAT could easily break through resistance and all the fundamental things we’ve been through and make new highs. I just don’t think that’s going to happen, and I think the odds are we’ll see lower prices before we see higher prices. For that reason, I’m changing the stock from Hold to Sell.

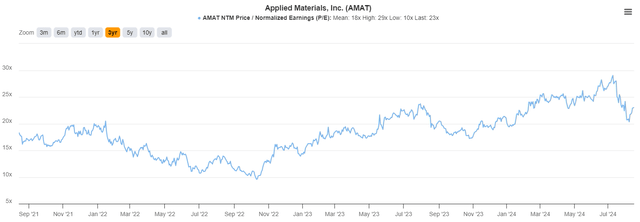

The stock now trades at about 23 times earnings, 5 percent above its three-year average, although it remains close to its low 2024 valuation so far.

TIKR

Given AMAT’s modest growth of late and for the foreseeable future, I can’t imagine paying 23x earnings. Valuations are always in the eye of the beholder, but for me there are better values. I would be interested in 18-20x earnings, but at 23 the risk is just too high.

In summary, Q3 results were good. Q4 guidance is good. I’m still concerned about whether long-term margins can support EPS growth, as revenue growth and buybacks are both only good for modest earnings gains. The price chart and seasonality suggest we’ll see $190 before we see $220. For this reason, I’m giving AMAT a sell rating. I’m NOT suggesting you get out and sell short; I’m just saying there are better opportunities for your money right now.