")

Thomas Barwick

I have published my “Strong Buy” thesis for Emerson (NYSE: EMR) in May 2024, signaling the company’s transition to a higher-growth industrial technology company focused on software, controls, sustainability, decarbonization and energy transition. The company released its Q3 Earnings on August 7, showing only 3% organic revenue and order growth. The share price took a hit after the earnings release due to weakness in maintenance, repair, and operations (“MRO”) and discrete automation. However, I think these issues are short-term challenges and I am buying into the weakness. I reiterate a Strong Buy rating with a one-year price target of $140 per share.

Weak MRO and discrete automation

During the earnings call, management highlighted the weakness in the MRO and discrete automation markets. Management expects a slow recovery in the discrete automation market, especially in the factory Automation, with stagnant to slightly positive growth expected in the fourth quarter.

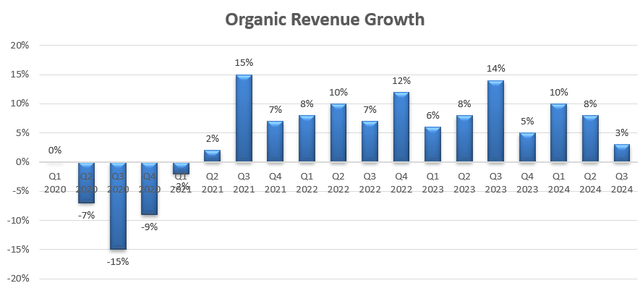

As a result, Emerson only achieved organic revenue and orders growth of 3%, as shown in the chart below. This represents a slowdown in organic revenue growth compared to recent quarters.

Emerson quarterly earnings

The reasons for the weak order development can be summarized as follows:

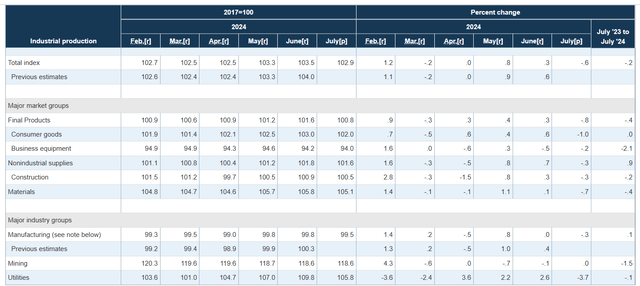

- During the quarterly earnings call, management noted that the current high interest rate environment has caused delays in some general industrial projects, resulting in weak demand for discrete automation and MRO. As shown in the table below, manufacturing production in 2024 has been quite weak due to the current high interest rate environment.

Federal Reserve Bank of St. Louis

- The automotive industry is an important end market for Emerson. Due to the weak consumer spending environment, automotive production in 2024 is down year-on-year. This decline in the automotive market has created growth challenges for Emerson’s discrete automation and test and measurement portfolios.

FRED

Growth forecast and valuation

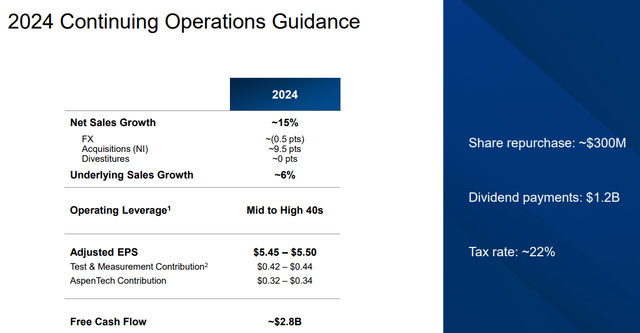

Emerson forecasts FY24 organic sales growth of 6% and acquisition growth of 9.5% (see slide below).

Emerson Investor Presentation

I consider the following factors for FY24 growth:

- Smart Devices: Since discrete automation accounts for about 20% of total smart device revenue, weakness in the general industrial market is expected to create growth challenges for the segment in fiscal 2024. I forecast discrete automation revenue to decline 1% in fiscal 2024, while other business lines, including final inspection, safety and productivity, and measurement and analytics, will grow 6%. Therefore, I expect the smart device segment to grow 4.6% in fiscal 2024.

- Software & Control: As mentioned in my previous article, Emerson has been expanding its software, services, and control systems business, which will provide recurring revenue to the company. I forecast the business to grow 10% in fiscal 2024.

I estimate that by combining the two segments, Emerson will achieve organic revenue growth of 6% in fiscal 2024. For the growth rate from fiscal 2025 onwards, I expect the Smart Devices business to recover to its historical growth rate of 6%, while Software & Control will grow by 10%. Therefore, the total growth rate from fiscal 2025 onwards is estimated at 7%.

On the margin side, I expect an annual margin increase of 20 basis points, driven by the following:

- 10 basis points of gross profit due to the introduction of new products

- 10 basis points from operating SG&A leverage

The DCF summary:

Emerson DCF

I calculate the free cash flow from equity as follows:

Emerson DCF

The cost of equity is calculated at 10%, assuming: risk-free rate 3.8% (yield on 10-year US Treasury bonds); beta 0.98; equity risk premium 7%. The one-year target price is calculated at $140 per share, based on my estimates, with all future FCFE deducted.

Main risk

During the earnings call, management highlighted the weakness in China that has impacted Emerson’s test and measurement business. Management lacks transparency on the recovery of the China business. In the next quarter, Emerson will provide guidance for fiscal 2025, and I expect they will provide cautious guidance for their China business in fiscal 2025, which could cause concern in the market.

Endnotes

Current high interest rates and a weak automotive market have created some growth challenges for Emerson in the near term. In my view, the discrete automation and MRO businesses will recover as the economy and interest rates moderate. I reiterate my Strong Buy recommendation with a one-year price target of $140 per share.