")

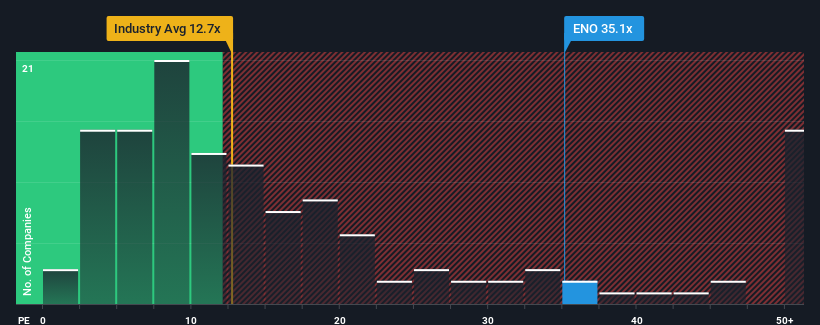

Elecnor, SAs (BME:ENO) price-to-earnings (or “P/E”) ratio of 35.1 might make it seem like a strong sell at the moment, compared to the Spanish market, where about half of the companies have P/E ratios below 19x, and even P/E ratios below 11x are quite common. Still, we would have to dig a little deeper to determine if there is a rational basis for the greatly elevated P/E ratio.

With earnings growth that has been better than most companies recently, Elecnor has done relatively well. It seems that many expect the strong earnings performance to continue, which has increased the P/E ratio. You really hope so, otherwise you’re paying a pretty high price for no particular reason.

Check out our latest analysis for Elecnor

Do you want the full picture of analyst estimates for the company? Then our free The Elecnor report will help you find out what’s on the horizon.

Is the growth appropriate for the high P/E ratio?

There is a fundamental assumption that a company must significantly outperform the market for P/E ratios like Elecnor’s to be considered reasonable.

If we look at last year’s earnings growth, the company posted a fantastic 20% increase. However, this was not enough as the last three-year period as a whole saw a very unpleasant 44% decline in earnings per share. Accordingly, shareholders were sobered about medium-term earnings growth rates.

According to the three analysts who cover the company, earnings per share are expected to grow 31% per year over the next three years. With the market only expecting a 15% annual increase, the company is poised for a stronger result.

With this information, we can see why Elecnor is trading at such a high P/E compared to the market. It seems shareholders are not interested in offloading something that potentially has a better future ahead of it.

The most important things to take away

It is argued that the price-to-earnings ratio is not a good measure of a company’s value in certain industries, but can be a meaningful indicator of business sentiment.

As we suspected, our study of Elecnor’s analyst forecasts found that its above-average earnings outlook is contributing to its high P/E ratio. At this point, investors believe that the potential for earnings deterioration is not large enough to justify a lower P/E ratio. Unless these conditions change, they will continue to provide strong support to the share price.

You always have to keep an eye on risks, for example: Elecnor has 1 warning sign In our opinion, you should be aware of this.

If you uncertain about the strength of Elecnor’s businesswhy not explore our interactive stock list with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we are here to simplify it.

Find out if Elecnor could be undervalued or overvalued with our detailed analysis, with Fair value estimates, potential risks, dividends, insider trading and the company’s financial condition.

Access to free analyses

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.