")

Umnat Seebuaphan

introduction

Opera Limited (NASDAQ: OPRA) and its subsidiaries offer browsers for mobile devices and PCs internationally. The company has three main browsers: Opera Mini, Opera One and Opera GX. With these browsers, Opera generates revenue through search and advertising.

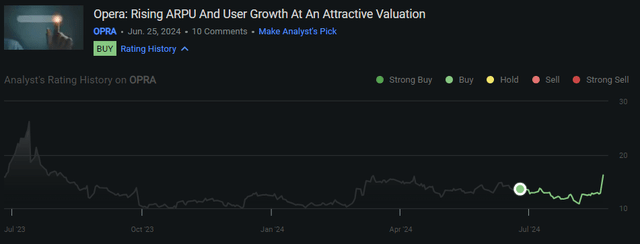

Analyst history for OPRA (Search Alpha)

The stock price has been quite volatile over the past year, fluctuating between lows of $10 and highs of $17. Since I wrote my last article, the stock has performed quite well, up 12%. Opera still has a lot of potential as sophisticated Western users continue to download and use its browsers.

Result update

The company just announced its second quarter 2024 results last week and surprised analysts with optimistic numbers. The company also raised its guidance for fiscal 2024, indicating that the company expects higher revenue from advertising and search. Below is a quick breakdown of the numbers:

- revenue increased by 17% year-on-year to 109.7 million US dollars

- Advertising revenue of $65 million, up 20% year-over-year

- Search revenue of $45 million, up 15% year-over-year

- Net profit of $19.303 million, an increase of 43% year-on-year

- EPADS of USD 0.22 (in the same period last year, EPADS was USD 0.15), thus meeting analysts’ expectations.

- Annualized Average revenue per user of $1.46, up 25% year over year

- Average number of users of 298 million, a slight decrease from Q1’24 (304 million)

Overall, I view the results as very positive, and the market seems to agree. Since the earnings announcement, the share price is up about 21% to $15.64. Total MAUs were down for the quarter, but seasonality is definitely at play here, with fewer people using browsers during the spring and summer. GX still saw stronger adoption, as management commented during the earnings call:

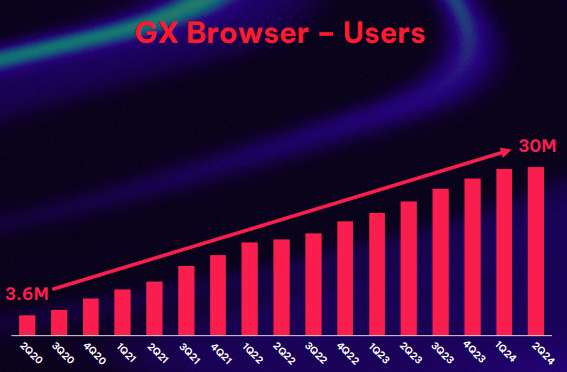

Although summer seasonality is taking a toll on our product, Opera GX added another 500,000 users during the quarter and surpassed 30 million MAUs, achieving 27% year-over-year user growth combined with ARPU growth now at 14% year-over-year and $3.55 on an annualized basis.

-Co-CEO Song Lin

Q2’24 Investor Presentation GX Users (Opera Investor Relations)

It’s good to see GX continue to grow even during tougher times of the year, as it shows that there is strong demand for the product during times when demand is usually lower. GX is still only used by less than 2% of all PC gamers, which presents huge growth opportunities as Opera can continue to improve and market its browser.

Continuous ARPU growth

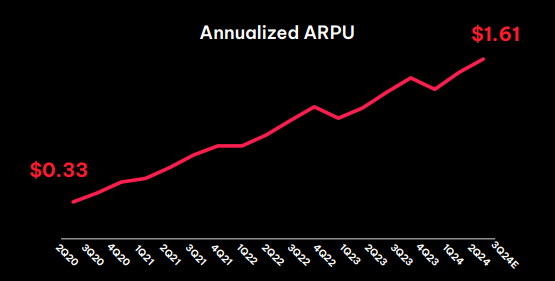

As I mentioned in my last article, ARPU was a key focus for management. The company’s gamer-focused browser, GX, was the key revenue driver as it targets the most monetizable audience. One of the first things said in the Q2 2024 earnings call was ARPU:

In addition to revenue above performance, our profitability benefited from (event title) (ph) focusing on the most monetizable users while evolving the portal in terms of our marketing spend. As a result, we were able to increase ARPU by 25% year-on-year and now average $1.46 per year across our products and geographies.

– Co-CEO Song Lin

ARPU has grown 4.5x over the last four years as Western markets have started to use Opera and its browsers more and more. I see no reason why this number shouldn’t continue to grow as the user base continues to grow and more Western users with monetizable revenue are using the platform due to the DMA.

Q2’24 Investor Presentation Annualized ARPU (Opera Investor Relations)

The company expects ARPU to grow 10% to $1.61 in the third quarter of 2024, with no signs of slowing down. GX’s success with gamers is an example of how to build a product around a user base, and the team at Opera has said it will continue to optimize the browser to give users the best possible search experience.

Google, OpenAI and the future of search

In its Q1 2024 results, the company said Google had exercised its option to extend the search contract through 2025, meaning Opera would continue to use Google as its default search engine for another year. This was good news because it shows that Google clearly views Opera as an important search partner. The deal also gave Google the option to extend the contract on current terms, suggesting that a new deal would require Google to pay Opera more.

This is where OpenAI comes in: About a month ago, OpenAI announced its latest offering, SearchGPT. Search engines like Bing and DuckDuckGo have struggled to compete with search giant Google, but OpenAI has big ambitions for its new AI search engine. OpenAI will need market share and people using their search engine to generate traffic. Combine this with the Google/Opera deal expiring next year, and it makes perfect sense for OpenAI to switch to Opera for search distribution.

Opera also feels like they are being ripped off and can get more for their market share. In response to a question about the antitrust case against Google and potential loss of search revenue, the company replied:

So at the end of the day, we don’t care if it (startup — whatever the revenue is) (ph). What matters to us is that we get paid. And as far as the high-level principle goes, I think everyone seems to be considering more and more that browser traffic, the default position in the browser is very relevant and very important. Actually more important than most people thought, then I think we should have the opportunity to get paid more, right?

– Co-CEO Song Lin

Whether Opera would actually change its engine is debatable, but the company absolutely believes it deserves better terms in a new contract. I would say the most important thing is that they do the right thing by their users. It would be a huge mistake if the company changed its engine only to see thousands or even millions of users churn due to dissatisfaction with the new engine.

Evaluation

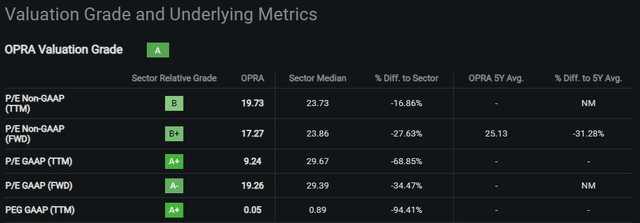

Despite the recent share price increase, Opera remains undervalued. The company currently trades at 17 times forward earnings, well below the industry average of 23.86. With revenue growth in the mid to low double digits, a P/E ratio of at least 20 would be expected.

Search for Alpha Rating for OPRA (Search Alpha)

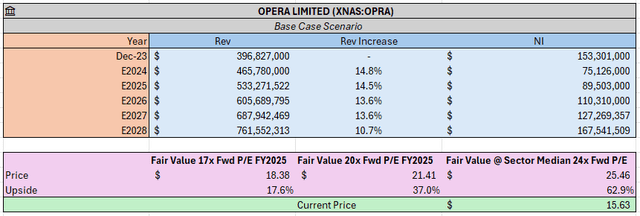

My model suggests a fair value of $21.41 if we conservatively use 20x fiscal 2025 earnings. If we use the industry median of 23.86x, we get a fair value of $25.46. The company is trading well below the industry median, but has much higher revenue growth than the sector.

Opera profit multiplier model (Author’s analysis, Seeking Alpha)

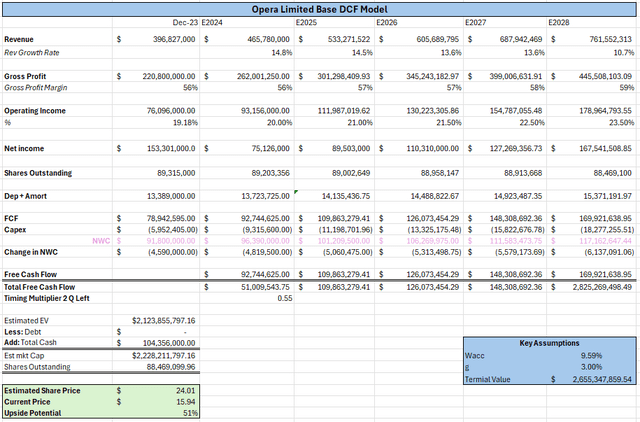

I have also built a DCF model for Opera, which again suggests that the company is undervalued at current prices. My model is based on the following assumptions:

- Revenue growth of 14.8%, 14.5%, 13.6%, 13.6% and 10.7% for 2024, 2025, 2026, 2027 and 2028 respectively

- Operating profit of approximately 76.1 million, 93.15 million, 112 million, 130.2 million, 154.8 million and 179 million for 2024, 2025, 2026, 2027 and 2028

- Diluted shares (ADS) outstanding of 88,469 million

- WACC of 9.59% (calculation included)

- Final growth of 3%

Opera DCF model (Author’s analysis, Seeking Alpha)

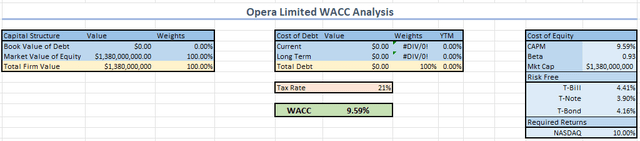

My WACC calculation can be found below:

Opera WACC analysis (Author’s analysis, Seeking Alpha)

Based on the stated assumptions, we get a fair value of $24.01, or an upside of 51% from current prices. Combine that with a 6% annual dividend yield, and I’m more than happy to hold the shares and continue to buy more as prices fall from their current levels.

I would also like to point out that I consider the numbers used to be quite conservative, as the company has consistently exceeded its revenue targets over the past 5 years. Taking all factors into account, I am raising my rating on Opera from Buy to Strong Buy with a price target of $24.01.

Dividend stability/concerns

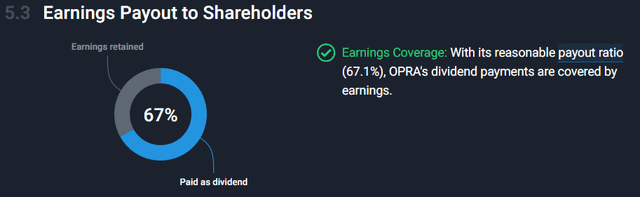

I really only have two major concerns about the company, one of which is its current dividend payout. I know I just said I’m OK with holding the stock knowing it has a 6% dividend yield, but I can’t help but be concerned about the current payout ratio. The current payout ratio is quite high, with 67% of net income being paid out as dividends. I realize the ratio will only go down as earnings continue to grow, but the company is only a few bad quarters or a one-time event away from no longer being able to reliably pay its dividends.

Opera’s dividend payout ratio (Just Wall St.)

In the Q1 2024 earnings call, CFO Frode Jacobsen said the best way to reward shareholders is through a dividend. That’s fair, but I’m still not sure why they decided on such a high amount to begin with. I would have been more than happy if the company had paid an annual yield of 3% and used the money that would have been used to pay the other 3% to buy back shares at a significantly reduced price.

Property

This leads to the next big issue, which I believe remains the biggest negative for the company. Kunlun still owns around 72% of the company, and many investors still fear that the connection to China is not a good thing.

Opera Ownership Details (Just Wall St.)

I repeat what I said in my last article: I don’t think this is a big deal, as the software division of the company is still based in Norway. Ultimately, the opinion of other investors will drive the share price up or down in the future.

Diploma

In conclusion, Opera shares are significantly undervalued. With a 6% annual dividend yield, strong revenue growth, and rising ARPU, the current valuation doesn’t make much sense. The potential for a lucrative search deal with OpenAI or an even better search deal with Google in the coming year adds to an already promising future. Given these factors, I expect Opera stock to soon command the premium it rightfully deserves. Now could be the ideal time for investors to take advantage of this opportunity before the market catches up.