")

Subscribe

introduction

I have given a “Strong Buy” recommendation for Enbridge (NYSE:ENB) in April. I am quite satisfied because ENB has delivered almost 13% total return to investors after my recommendation. My updates to fundamental and valuation analysis suggest that it There is no reason to be less optimistic about ENB and I reiterate my Strong Buy rating.

The long-term outlook for the U.S. economy is positive, which benefits the energy midstream industry. As the industry’s largest player, Enbridge should also benefit from accelerated data center investments. The recent release of second-quarter results adds significantly to my optimism as profitability continues to rise, helping to maintain a healthy balance sheet, which ultimately increases dividend safety. Recent acquisitions suggest that management wants to strengthen ET’s position as one of the most important companies for the U.S. energy sector. Valuation remains compelling, and a high dividend yield of 6.9% is expected. is safe. Preference shares such as Enbridge Inc. CUM RED PF SL (OTCPK:EBBNF) is also quite interesting as it offers a dividend yield of 7%.

Fundamental analysis

I think Enbridge’s appeal lies in the 6.9% dividend yield the stock offers. This seems particularly attractive in the current situation where the stock market is extremely fearful, weighing on sentiment toward growth stocks. Shares of all major technology companies are falling, and 2022 has taught us that even prominent and highly profitable tech giants can experience massive sell-offs. In this situation, shares of dividend machines like Enbridge are likely to thrive.

For readers who have not heard of Enbridge, here is a brief summary of why the company is an important part of the overall North American energy system. Enbridge has a diverse portfolio of energy businesses: pipelines and terminals that facilitate the transportation of liquid hydrocarbons. In addition, Enbridge also owns and operates gas gathering, processing and distribution facilities.

Enbridge

My confidence is primarily based on the company’s massive presence in an industry as strategically important for any country as the energy midstream industry. In this industry, new technology could not lead to a faster and cheaper way to transport hydrocarbons within North America’s vast energy infrastructure network. Nevertheless, I believe that Enbridge’s strategic positioning is intact.

S.A.

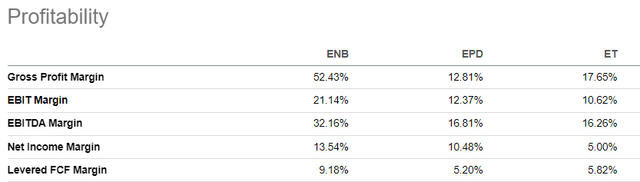

Enbridge is the largest midstream company in North America with a market capitalization of $84 billion. Its largest competitors in terms of market capitalization are Enterprise Products Partners LP (EPD) and Energy Transfer LP (ET). Among these three competitors, ENB has by far the highest profitability in all metrics.

S.A.

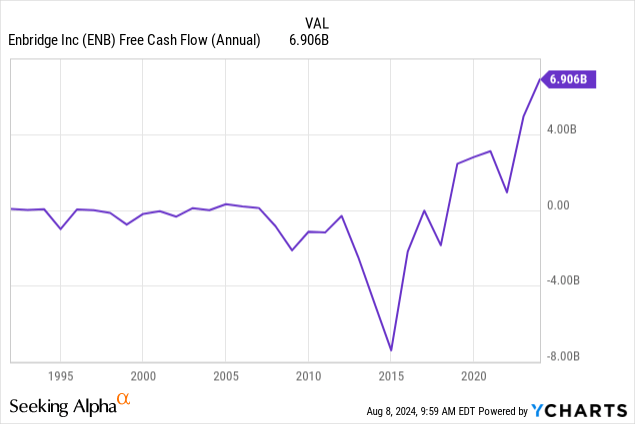

I think management is consistently focused on creating more value for shareholders, and the recent second quarter earnings release confirmed this once again. Although revenues were almost flat in the second quarter compared to the same period last year, Enbridge posted solid growth in EBITDA and distributable cash flow. An improving profitability profile is a strong bullish indicator for dividend investors.

Enbridge

Other bullish factors from the second quarter earnings release include management increasing its full-year EBITDA guidance and reaffirming its commitment to maintaining capital allocation discipline and a strong balance sheet. Management expects full-year EBITDA to be approximately $18 billion, up 9% from fiscal 2023.

Enbridge

The overall environment appears favorable for Enbridge to maintain its impressive financial performance trajectory. Steady growth in energy demand depends on the overall health of the economy, meaning demand for hydrocarbons is likely to increase as economic activity increases. The quantitative measure of economic activity is gross domestic product (“GDP”). According to Deloitte, U.S. GDP is expected to show steady real growth of around 2% through 2028.

Deloitte

The current new phase of the digital revolution is another tailwind for the industry. According to TC Energy’s executive vice president and chief operating officer of natural gas pipelines, gas demand to power data centers will increase by as much as 8 billion cubic feet per day by 2030. Since energy must be transmitted before it is consumed by data centers, this factor is also a solid long-term tailwind for Enbridge.

Valuation analysis

ENB did not look cheap to me when I first looked at the comparison of its valuation multiples with its North American midstream peers below. Enbridge has much higher P/E ratios (various periods). On the other hand, as an investor looking for a high dividend yield opportunity, cash flows are much more important to me than book profits and accrual. Therefore, I would like to ask readers to pay attention to the last row in the table below. From price to cash flow, Enbridge does not look expensive compared to its peers. Also, please remember that ENB is the most profitable among its closest peers.

S.A.

I commend ENB for its generous dividend payouts, which leaves me no choice but to examine its valuation using the Dividend Discount Model (“DDM”). The formula is discounted at a rate of 7.15%, which is ENB’s cost of equity. The current dividend is the annual TTM payout, which was $2.66. I think using a 2% dividend growth rate for my analysis seems to be a reasonable choice as it is consistent with long-term inflation rates.

Calculated by the author

ENB’s fair value is $51.65. I like the valuation because a fair share price of nearly $52 means there is around 34% upside potential. The upside is certainly compelling. Please also remember that the stock offers what I believe is a 6.9% dividend yield.

Mitigating factors

Enbridge owns and operates tens of thousands of miles of pipelines that carry highly flammable liquids and pose potential environmental hazards in the event of leaks and subsequent spills. Therefore, the company’s ESG risks are significant. Environmental incidents are likely to result in fines, cleanup costs, and even legal liabilities. These are the potential direct factors that could impact Enbridge’s financial performance. Apart from that, there is an indirect effect. Potential leaks and spills can damage Enbridge’s reputation and undermine stakeholder confidence. This could indirectly impact shareholder returns.

In addition to the ESG risks associated with physical damage to the pipeline, even a small technical issue in a relatively small section of the pipeline can result in downtime for the entire branch. The company’s financial success depends significantly on the physical condition of its properties, facilities and equipment. This means that Enbridge must proactively undertake maintenance and repairs, and any unexpected downtime can be costly to shareholders.

Although Enbridge is a midstream company that does not sell crude oil, its financial success is vulnerable to cycles in the energy commodity markets. The company experienced a massive decline in its free cash flow in 2014-2015 when commodity prices (particularly oil and gas) fell sharply as a result of the shale oil revolution. Since oil and gas markets are inherently volatile, it could potentially experience a sharp decline in commodity prices and Enbridge’s cash flows would likely suffer as well.

Diploma

ENB and EBBNF’s excellent dividend yields of around 7% remain safe as fundamentals are rock solid and management’s commitment to maintaining capital allocation and financial discipline increases the certainty of distributions to shareholders. Accelerated data center investments by tech giants are a strong long-term tailwind for ENB. Valuation remains attractive, meaning ENB is still a “strong buy.”

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.