")

Richard Drury

Investment thesis

IBM (NYSE: IBM) (NEOE:IBM:CA) is one of the oldest companies on the market, having passed many tests of time and experienced everything, and having already gone public before the end of the First World War. As a result, the company has seen many technologies come and go. It has pioneered some of these technologies over the past few decades, such as the floppy disk, the mainframe, and the personal computer, while it missed the boat on some important technologies, such as the smartphone and cloud computing.

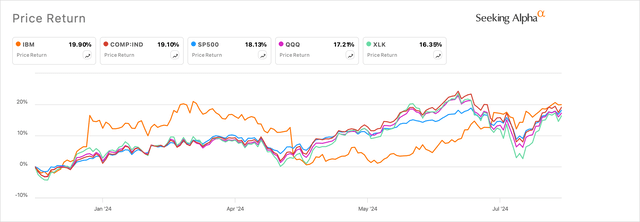

It was IBM’s missed innovation train that cost the company dearly and left most of its investors with major bruises. This was especially evident over the last decade, when IBM stock lost 32% between 2010 and 2019 while the S&P 500 gained 123%, causing many investors to become extremely sour on Big Blue.

However, IBM’s new management has repeatedly demonstrated its ability to steer the company through challenges and opportunities, setting the company on course to beat the S&P 500 this year.

Appendix A: IBM shares compared to leading indices and benchmarks (Search Alpha)

Examples of such opportunities include IBM’s software and GenAI businesses, which are growing faster than the company itself and account for an increasingly large share of the company’s total revenue.

The company is still viewed with some skepticism by many market participants and I am convinced that it would be beneficial for investors to take advantage of this pessimism given the growth trajectory to date.

I still recommend buying IBM.

GenAI and software business create growth opportunities for IBM

In my last coverage of IBM, I explained how IBM’s software and consulting businesses were beginning to reignite IBM’s old, dusty growth engines for the first time in years.

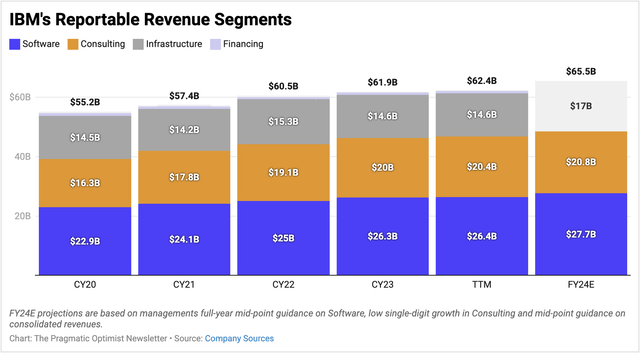

While consulting has not shown its full strength as expected, the software business has more than offset the stagnant growth in consulting. IBM’s second quarter results show that total revenue continued its single-digit growth pace, increasing 2% year-over-year to $15.8 billion. On a TTM basis, this represents a ~3.7% compound annual growth rate since 2020. But after factoring in management’s mid-single-digit growth estimates for 2024, IBM is expected to post ~$65 billion in revenue in 2024. This should translate to a ~4.4% compound annual growth rate of IBM’s total revenue since 2020, the year IBM’s new CEO was appointed.

Appendix B: IBM revenue compared to estimates by reportable segment (Company documents)

At the heart of IBM’s performance to date is the company’s software business, which includes its TP or transaction processing solutions and its hybrid cloud platform solutions. The company usually refers to its TP business as a “value vector” because it is a high-margin business for the company. IBM has been able to benefit greatly from strong mainframe cycles since 2022, which has led to a turnaround in IBM’s TP business and expanded the boundaries for the entire software business segment.

However, the bigger and long-term growth driver for IBM has been the hybrid cloud platform business, with the acquisition of Red Hat in 2019 still accounting for a large portion of the growth. Red Hat and Automation are growing together in the high single-digit and double-digit ranges, respectively, led by strong growth in the hybrid cloud business at Red Hat and OpenShift, as well as on the Watsonx AI Platform side.

What the company has done well in GenAI’s current global innovation cycle is to bring its AI capabilities to market quickly and build partnerships with its competitors. “Strengthening the position of the established computer manufacturer in the AI race.” These partnerships include IBM’s work with Meta Platforms (META), Amazon (AMZN), Adobe (ADBE), and Microsoft (MSFT), among others. Given the strength already evident in the software business, management now expects this business to grow at a high single-digit rate in 2024, which is quite strong given IBM’s history over the last decade.

While the company is experiencing some pressure in its consulting business due to lower IT spending, digital transformation projects are particularly attractive, which continues to keep demand for IBM’s consulting services at a moderate level. The company’s book-to-bill ratio remains above 1.15. Management expects the consulting segment to stagnate over the course of the year.

I believe that management could easily achieve its mid-single-digit growth targets for the year, as it occasionally “prudent.”

Software and AI increase margins and increase free cash

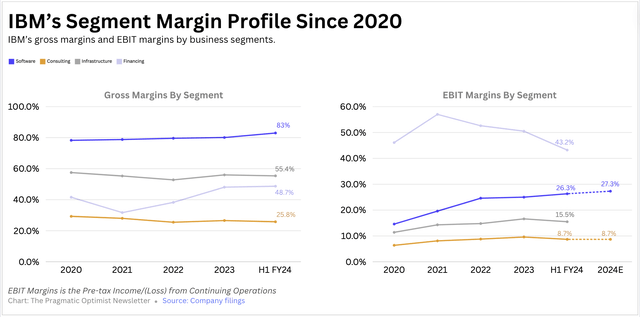

The strength of IBM’s software and GenAI businesses is impacting operating leverage, where margins continue to expand.

At the corporate level, IBM’s gross margins increased 180 basis points to 56.8 percent (according to the 10-Q), one of the highest gross margins Big Blue has reported in recent years. The main growth driver for the rising margins was IBM’s software business, which increased 150 basis points to 83.6, as shown in Exhibit C.

Appendix C: IBM’s margin profile by reportable business segments (Company documents)

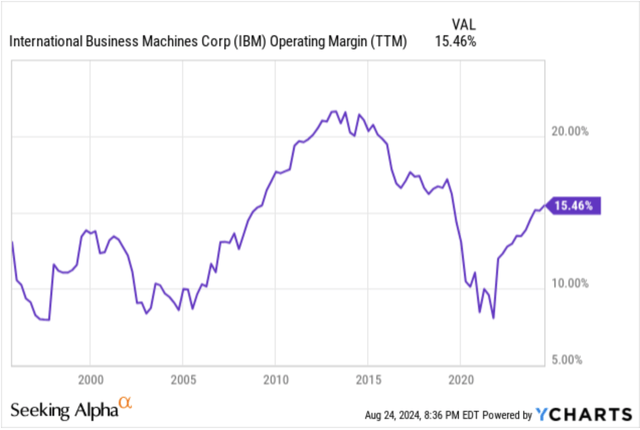

Further analyzing at the segment profit or EBIT level, management reported that just over a quarter of the software business was recorded as segment profits. Additionally, due to the progress and operating leverage, they believe that segment profit margins in the software business can increase by a full one percent this year. At the organizational level, the company reports an increase in GAAP operating margins, putting the company back on track for expansion.

Exhibit D: IBM’s operating margin expansion continues on a TTM basis (YCharts)

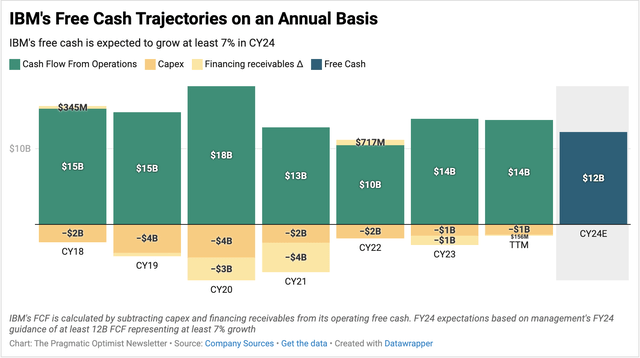

The growth in operating margins has encouraged management to modestly raise its free cash flow targets for fiscal 2024 to at least $12 billion, after recording $11.2 billion in free cash last year, implying expected free cash growth of ~7.2% year-over-year this year. Additionally, investors should note that management has become more efficient in providing free cash by better managing its capital expenditures and other payable items, as seen in Exhibit E.

Exhibit E: IBM’s free cash components and growth curve. (Company documents)

Valuation shows that IBM’s free cash growth is not taken into account

Using a reverse DCF valuation model, I see that markets are currently pricing in almost no free cash growth over the next ten years. As astonishing as that is, I believe it is simply because analysts are extrapolating current results and arriving at no future free cash growth.

Appendix F: IBM’s valuation model points upward (Author)

To explain even more precisely, since IBM already has ~$12.3 billion in free cash on a TTM basis, analysts believe there will be no free cash growth for the rest of the year and extrapolate that scenario. In my opinion, that is short-sighted and I believe that with the strength IBM has already shown, the company should deliver at least 2-4% free cash growth over the next 10 years.

Additionally, free cash growth of 2-4% is closer to management’s single-digit long-term growth model. Additionally, management has previously described its guidance as “prudent” or conservative, meaning it has plenty of room to increase its guidance in the future. Based on long-term growth of 2-4%, I estimate IBM’s target to be around $223, implying around 14% upside.

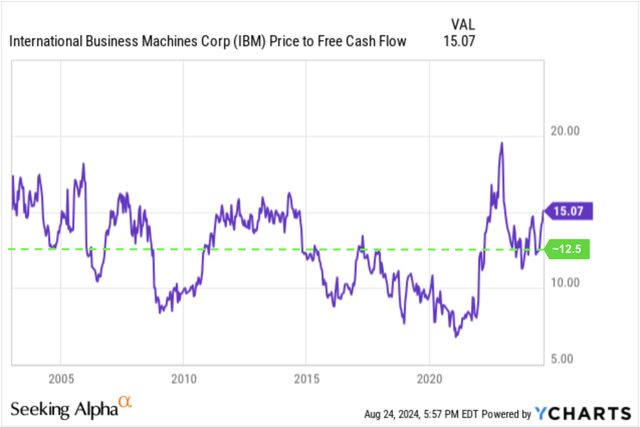

Some investors may be waiting for IBM to pull back from its post-Q2 earnings rally as of July 24. For those investors, I would recommend watching IBM’s Price/FCF valuation multiple, which is currently at ~15x. Those investors may be waiting for IBM’s Price/FCF multiple to pull back to ~12.5-13x, which represents a ~13% decline from IBM’s current levels.

Exhibit G: IBM’s price-earnings ratio is moderately elevated. (YCharts)

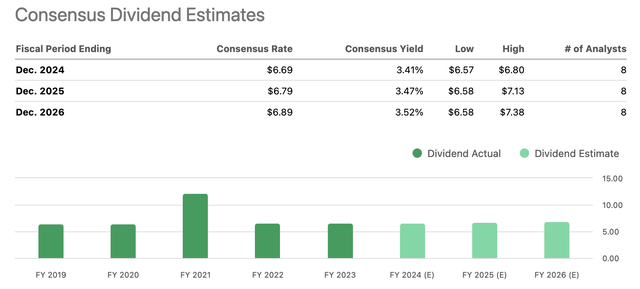

Still, IBM’s long-term growth seems severely underestimated and the company’s stock undervalued at current levels. At the same time, investors should keep in mind that IBM continues to offer one of the best dividend yields for a company that is restarting its growth engine. With a payout ratio of ~72%, IBM’s dividend looks extremely stable, and consensus estimates call for moderate dividend growth at IBM.

Appendix H: IBM Dividend Outlook (Search Alpha)

Risks and other factors to consider

While IBM’s software business has been a growth driver, as I mentioned in my post, IBM’s consulting business has been a moderate drag on growth after posting some growth last year. Management has pointed the finger at weak discretionary budgets in the IT sector, which can be attributed to the higher allocation of IT budgets to GenAI and AI proof-of-concepts, which has benefited IBM’s software business.

I reported on Accenture (ACN) a week ago and found similar signs in its consulting business. Accenture management has called for cuts in IT spending next year. Signs of cuts in the consulting world would be critical for IBM’s consulting business.

Take away

IBM continues to defy skeptics and build on the momentum it has built over the past few years. The company’s software business and GenAI solutions are giving wings to the company’s growth engine. Combined with the operating leverage management is showing, IBM is on track to deliver growth beyond what pessimists think growth will be.

I continue to recommend a buy rating for IBM.