")

winhorse/iStock Unpublished via Getty Images

overview

SoftBank Group Corp. (OTCPK:SFTBF) (OTCPK:SFTBY) is a holding company that invests in technology companies. Although its current strategy is focused on AI companies, it has invested in all relevant industries within technology. Space. Its portfolio includes public and private companies, a mix of a large technology investment fund and a venture capital firm.

Figure 1: Seeking Alpha

Over the past month, it has lost 15% of its value, reaching a high of 30% on August 5. This decline is a good investment opportunity because it is trading at a large discount to its net asset value per share. It is a way to invest in promising private companies, and it has launched a share buyback program that can further increase the share price.

High discount compared to net asset value per share

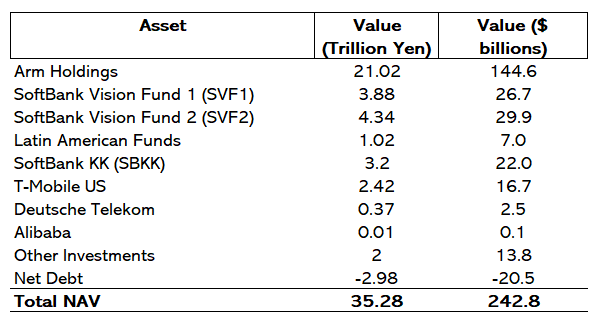

SoftBank is worth more than Total assets as an integrated company. If you consider only T-Mobile and Deutsche Telekom, the combined fair value is $19 billion. T-Mobile is worth $17 billion and Deutsche Telekom is worth $2.5 billion.

Figure 2: Author based in SoftBank’s earnings figures for the first quarter of fiscal year 2024

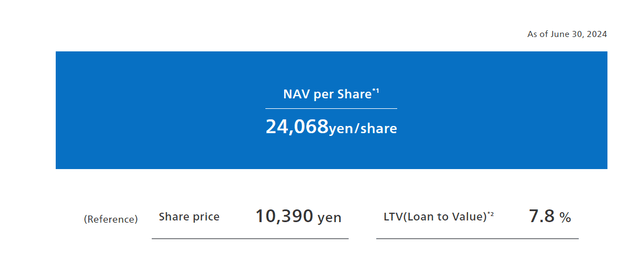

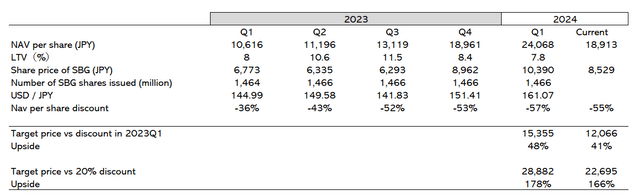

Using SoftBank’s latest reported net asset value per share, Figure 3, is ¥24,068 ($165.6). The current price is ¥8,529 ($58.7), so the value of the entire company is less than the sum of all the fair values of its investments. That represents a significant discount. Let’s examine whether this is an investment opportunity or if we’ve missed something.

Figure 3: Earnings figures for Q1 FY2024

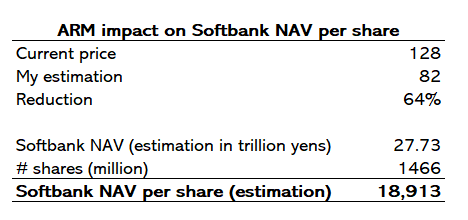

ARM is a decisive advantage in Valuation of SoftBank. In an article I wrote about the company, Beyond The Surface: What Made Me Buy Arm Holdings, I valued the company at $82 per share. Since then, the stock has risen to $128 per share. In the recent market crash, the price reached $107. So I’m still a bit more conservative and assign a value of $82. So, if I make the adjustments I just mentioned, SoftBank’s net asset value is 27.7 trillion yen ($190.8 billion) based on ARM holdings worth 13.4 trillion yen (64% of the original valuation in Figure 4, which is $92.2 billion). So my estimate of the discount is 55%, which is a bit more conservative than other sources.

Figure 4: Author

So with a conservative adjustment we can say that there is a discount and you can get all SoftBank investments at a discount.

A tool for buying private technology companies

Through Vision Fund 1 (SVF1), Vision Fund 2 (SVF2) and Latam Fund SoftBank reaches private tech companies that it could not otherwise reach. These companies can have high growth expectations, as is the case with Alibaba. Alibaba’s costs for SoftBank was 20 million dollars and got a maximum of 100 billion dollars. If you invest in SoftBank invests in popular companies like Flipkart and DiDi Global, giants in their respective industries and regions with extensive customer bases and significant market influence. Another example is Grab Holdings, a household name in Southeast Asia, or PicsArt, which is used by a wide range of people around the world, especially in the creative and social media communities. Despite this popularity, you don’t know how profitable these companies will be.

With the NAV discount that I analyzed earlier, I see SoftBank’s investment was to buy ARM and telecom companies (a total NAV per share of 11,008 yen, or $76.3 if you consider my ARM valuation of $82 per share) and get all the other companies for free. So I see double value: you get companies you couldn’t invest in on your own, and secondly, you get them for free.

Share buyback program

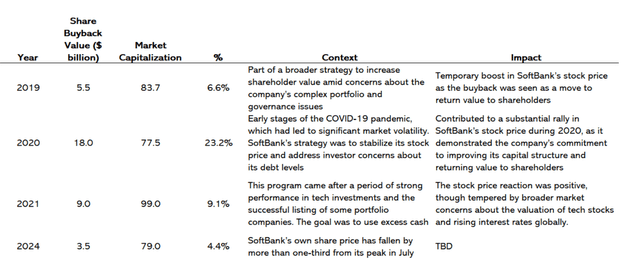

Figure 5 compares SoftBank’s share repurchase programs from 2019 to 2024, with a focus on size, market impact and rationale for each repurchase. In 2019 SoftBank initiated a share buyback worth $5.5 billion, or 6.6% of its market capitalization. The move was intended to increase shareholder value amid concerns about the company’s complex portfolio. The buyback led to a temporary increase in SoftBank’s share price.

Figure 5: Author

In 2020 SoftBank announced a much larger share buyback worth $18 billion, covering 23.2% of its market capitalization. This happened during the COVID-19 pandemic when markets were very volatile. The buyback was aimed at stabilizing the stock, which led to a strong recovery in the company’s share price.

In 2021 SoftBank launched a $9 billion buyback, equivalent to 9.1% of its market capitalization, following a strong performance in technology investments. This program aimed to use excess cash from successful investments. In 2024 SoftBank announced a share buyback worth $3.5 billion (4.4 percent of market capitalization) in response to a sharp drop in its share price. Some activist investors such as Elliott Management have called for a larger program of up to $15 billion, the second-largest program with a capitalization of 20 percent.

Evaluation

We can assume that a holding or conglomerate firm will have a discount to value compared to a more focused firm. Studies have found that the conglomerate discount has persisted over time, with estimates ranging from 5% to 20% depending on the sample, time period and method used. The main theoretical explanations for the conglomerate discount are inefficient internal capital allocation, agency problems, increased organizational complexity and information asymmetry between the conglomerate and investors. Empirical evidence from Custodio, Colak and Hoberg generally supports these mechanisms as drivers of the discount. The more conservative scenario would be to consider a 20% discount. SoftBank is not a broadly diversified company because its focus is on technology and especially AI, so the more accurate discount should be less than 20%.

As I calculated in an earlier section, my estimate of net asset value per share is ¥18,913 ($130.1). As shown in Figure 6, in Q1 2024 SoftBank’s NAV per share discount is 57% according to my estimate, and the current price is -55%. You can observe that this discount was 36% in Q1 2023, which was not that long ago. So if I apply this discount to my NAV per share estimate, you get a target price of ¥12,066, which is a 41% premium to the current price. If instead of a 36% discount, I apply the 20% “conglomerate discount” I just mentioned, this premium is 166%.

Figure 6: Author

Therefore, I expect a significant premium of 41% over the current price, which I consider to be a good opportunity before conducting a risk analysis.

Risks

The main risk is to continue making wrong capital allocation decisions. Most companies in which SoftBank investments are risky and do not guarantee positive free cash flow, so these companies will destroy value. This part of the SoftBank is like public venture capital. To be a good VC manager, you have to trust the management.

The performance of SoftBank has not been very successful as a venture capital firm. In Vision Fund 1, the company was able to raise $100 billion, but in Vision Fund 2, most of the funds come from SoftBank itself. In other words, Vision Fund 1 did not perform as expected and investors did not want to participate in a new round of financing. This is part of the argument for why SoftBank’s net asset value is at such a discount. The capital allocation was not too smart. I believe that with such large amounts of money, you have to “invest in everything.” Why pick and choose ideas when you have almost as much money as you want? You must think that small companies don’t need large amounts of money right away. The venture capital market has different dynamics.

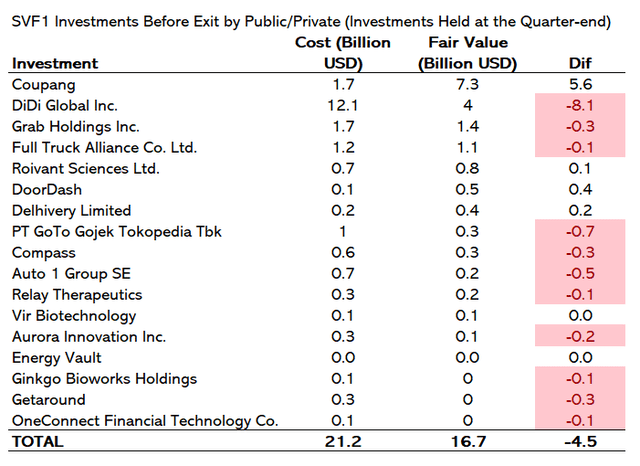

This misallocation of capital can have significant consequences. In the case of WeWork, this was a loss of $14 billion, about 5% of net asset value. In Figure 7, you can see how investments like Coupang were successful, but also other failures like Didi Global. Overall, it was negative.

Figure 7: Author based in SoftBank’s earnings figures for the first quarter of fiscal year 2024

SoftBank’s strategy is based on taking advantage of the AI era. This means that most of the investments made or to be made will go to AI companies. This is a good strategic decision, but today the most important companies in the AI space that are creating the leading platforms on which AI will work are Windows and OpenAI, Google, Amazon with Anthropic and Elon Musk’s xAI. And SoftBank has no presence in any of these companies.

Finally, there is the other main risk, currency risk. SoftBank is a Japanese company and you are investing in two assets: the company and the currency. Even if you invest in a U.S. stock market via arbitrage, it is like investing in the Japanese market. Foreign exchange markets are difficult to predict, so I can’t make an educated guess about the direction of the yen, which is why I discuss this in the risks section.

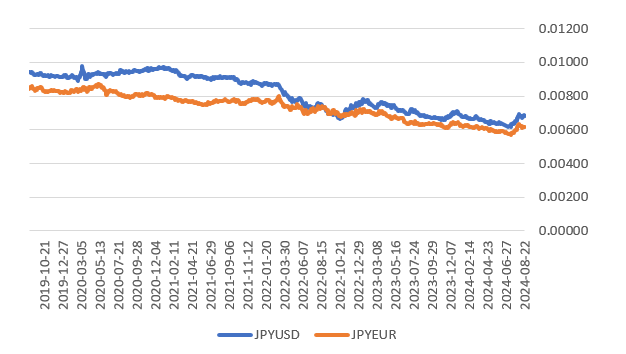

Figure 8 shows the yen’s performance against the dollar and the euro. The yen has depreciated against the US dollar in particular due to different monetary policies, different economic growth rates and market sentiments. However, this could change with changes in the global financial situation or adjustments to the BoJ’s domestic policy, especially if it could appreciate in the event of the expected interest rate cut in the US.

Figure 8: Author

This problem is a risk, but if the yen appreciates, it could become a good opportunity. Some well-known investors, such as Warren Buffett, have invested in the country.

Diploma

SoftBank offers a strong investment opportunity due to its significant discount to net asset value per share, potential returns from private technology investments, and an active share buyback program. This opportunity allows you to buy shares at a 55% discount, especially given valuable assets like ARM and telecom holdings. The company focuses on high-growth areas like AI and the opportunity to invest in promising private companies through its Vision Funds.

However, certain risks must be taken into account. SoftBank has struggled with capital allocation in some of its technology investments, leading to mixed results. The significant discount may reflect concerns about those past decisions.

Editor’s Note: This article discusses one or more securities that are not traded on a major U.S. exchange. Please be aware of the risks associated with these securities.