Andrew Harnik/Getty Images News

All eyes will be on Jackson Hole later this week and what Jay Powell has to say about the path of monetary policy. Meanwhile, the week’s more important speaker could arrive hours before Powell’s appearance. the stage and more than 5,000 miles away when Bank of Japan Chairman Kazuo Ueda appears before the Japanese parliament.

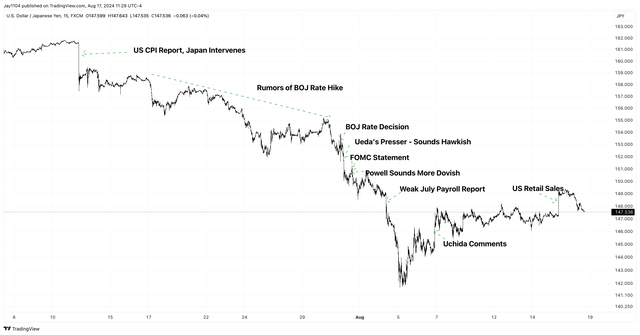

The Japanese yen and the carry trade, borrowing in a low-interest currency to invest in a higher-interest currency, have been making headlines in recent weeks as the USD/JPY, the exchange rate between the U.S. dollar and the Japanese yen, has fallen sharply, a sign that the U.S. dollar is weakening against the Japanese yen. The yen began to rise after the July 11 U.S. CPI report came in weaker than expected and the Japanese government subsequently intervened in the foreign exchange market. The USD/JPY continued to fall as Fears grew that the BoJ might raise interest rates in its monetary policy decision in July.

This was followed by weak US jobs data on August 2, which sent USD/JPY plummeting, leading to a decline in risk assets globally. The only thing that seems to have saved USD/JPY from an even steeper decline was the signal from BOJ Deputy Governor Uchida that the bank was downplaying the hunt for further rate hikes during this period, while also hinting that the bank would not raise rates during times of market volatility.

TradingView

Governor Ueda has been summoned to parliament to discuss the bank’s decision to raise interest rates on July 31 and the way forward. The question is how he will speak during that meeting and whether he will signal that there is likely to be further rate hikes in the future. That has generally been the view, but some wonder whether recent market volatility will prompt him to reverse some of his decision.

To create even more confusion Prime Minister Kishida has decided not to run for re-election and there are fears that political actors who could fill the vacuum may have views that are more supportive of the yen, which would mean that the USD/JPY move down.

While most attention is focused on the BOJ’s decision to raise interest rates, it is important to remember that all this started because of the weak US consumer price index (CPI) in mid-July and became worrying after the US jobs report in early August.

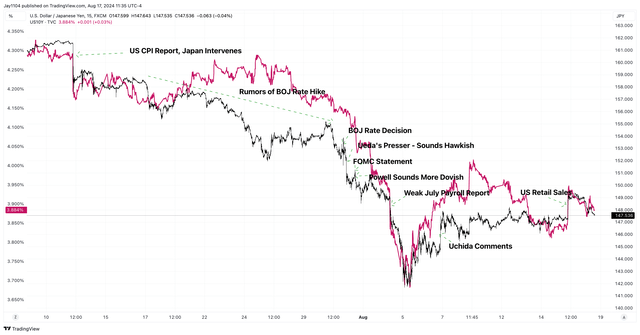

It almost seems like weaker US economic data and the Fed’s potential policy stance are playing a role, rather than the BOJ’s actions. The USD/JPY has tracked the US 10-year Treasury rate throughout the rapid decline. Was the BOJ’s rate decision part of the yen’s strengthening? Sure, but looking at the US 10-year rate’s trajectory, the US data seems to play an even bigger role.

TradingView

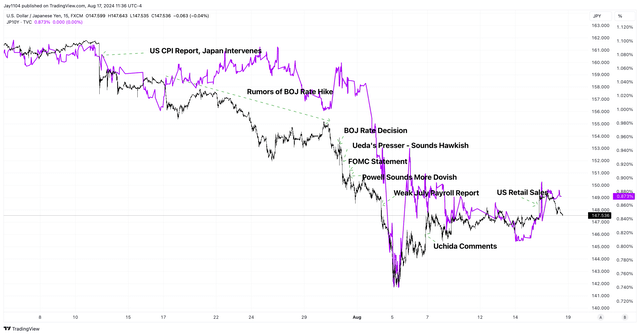

Since the spread between U.S. and Japanese interest rates has been narrowing throughout this period, the strengthening of the Japanese yen is likely due to this narrowing of interest rate differentials.

TradingView

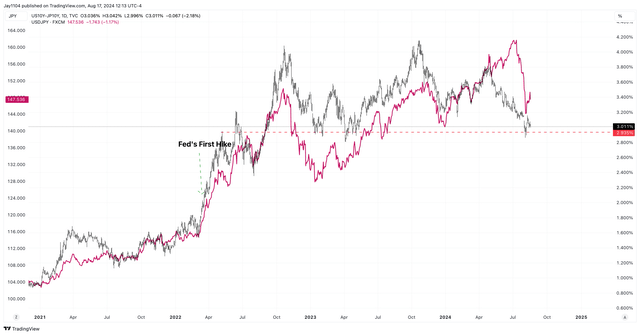

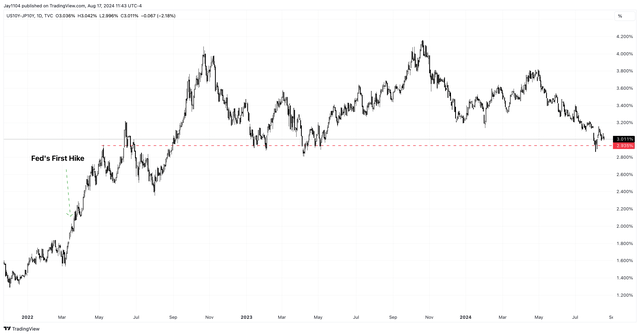

This USD/JPY and interest rate differential game has been going on since March 2022, when the Fed first raised rates. The USD/JPY and interest rate differentials between US and Japanese rates have been intertwined ever since. With the Fed now entering a potential rate-cutting cycle and the BOJ still in the midst of a rate-hiking phase, these differentials are only likely to continue to narrow.

TradingView

It appears that the technical support for the 10-year US interest rate minus the 10-year JGB is at a 2.9% spread. If the range falls below this support level, it could lead to a further narrowing of the spread, which could strengthen the yen further and push USD/JPY even lower.

TradingView

However, this is a double-edged sword. What the market needs now to prevent this trade from falling apart even further is a more dovish-sounding Ueda (who favors fewer rate hikes) and a more hawkish-sounding Powell (who favors not cutting rates too quickly). This would allow USD/JPY to move higher as the interest rate spread is likely to widen.

At this point in time, given the continued decline in inflation, the weakening labor market, the Fed’s preparations for rate cuts and the BoJ’s rate hikes, it is likely that the yen will continue to strengthen over time. And that will not have a positive effect on risky assets in general, given the continued unwinding of carry trades.