doesn’t tell you")

SD Biosensor, Inc (KRX:137310) shares have had a really impressive month, gaining 25% after a shaky period earlier. Despite the recent rise, the annual share price return of 4.6% is not that impressive.

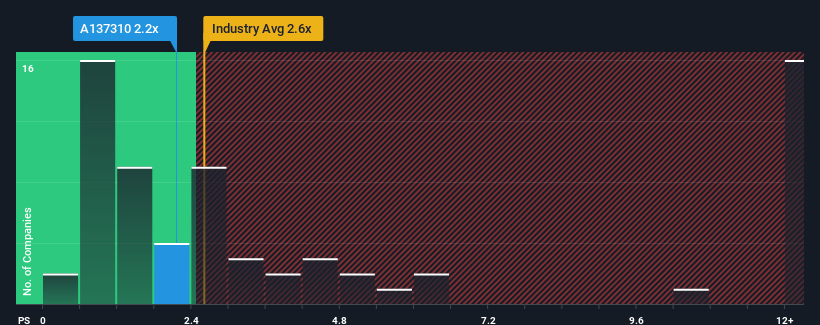

Although the price has risen sharply, it is not an exaggeration to say that SD Biosensor’s price-to-sales ratio (or “P/S”) of 2.2 seems fairly “average” at the moment, compared to the medical device industry in Korea, where the median P/S ratio is around 2.6. However, it is not wise to simply ignore the P/S without explanation, as investors may miss a special opportunity or a costly mistake.

Check out our latest analysis for SD Biosensor

This is how the SD Biosensor has proven itself

For example, let’s say SD Biosensor’s financial performance has been poor recently as revenue has been declining. One possibility is that the P/S ratio is modest because investors think the company could still do enough in the near future to keep up with the broader industry. If not, existing shareholders may be a little concerned about the profitability of the share price.

Although there are no analyst estimates for SD Biosensor, take a look at these free Data-rich visualization to see how the company is performing in terms of profit, revenue and cash flow.

Do the sales forecasts match the P/S ratio?

There is a general assumption that a company should follow industry trends for P/S ratios like SD Biosensor’s to be considered appropriate.

First, if we look back, the company’s revenue growth last year was not exactly exciting as it recorded a disappointing 40% decline. This means that there has been a decline in revenue over the long term as well, with revenue declining by 81% overall over the last three years. Therefore, it is fair to say that the revenue growth of late has been unwelcome for the company.

In contrast to the company, the rest of the industry is expected to grow by 31% next year, which puts the company’s recent medium-term sales decline into perspective.

With this in mind, we find it troubling that SD Biosensor’s P/S exceeds that of its industry peers. It appears that many of the company’s investors are far less pessimistic than its recent history would suggest and are not willing to offload their shares at this time. Only the bravest would assume that these prices are sustainable, as a continuation of recent sales trends will likely weigh on the share price at some point.

The most important things to take away

Shares have risen significantly and SD Biosensor’s price-to-sales ratio is now back in the range of the industry median. It is argued that the price-to-sales ratio is a poorer indicator of value in certain industries, but can be a meaningful indicator of business sentiment.

Our look at SD Biosensor has shown that declining revenues in the medium term have not affected the P/S as much as expected, as the industry is geared towards growth. When we see a decline in revenues in the context of rising industry forecasts, it makes sense to expect a possible decline in the share price on the horizon, driving the modest P/S down. Unless the circumstances of the recent medium-term performance improve, it would not be wrong to expect a difficult time for the company’s shareholders.

You should also inform yourself about these 3 warning signs we discovered with the SD Biosensor (including 1 that is a bit uncomfortable).

Naturally, Profitable companies with a history of strong earnings growth are generally safer bets. You may want to see this free Collection of other companies that have reasonable P/E ratios and strong earnings growth.

New: Manage all your stock portfolios in one place

We have the the ultimate portfolio companion for stock investors, and it’s free.

• Connect an unlimited number of portfolios and see your total amount in one currency

• Be notified of new warning signals or risks by email or mobile phone

• Track the fair value of your stocks

Try a demo portfolio for free

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.