doesn’t tell you")

Northwest Pipe Company (NASDAQ:NWPX) shareholders have been rewarded for their patience with a 25% jump in the stock price over the past month. The last 30 days bring the year-to-date gain to a very respectable 46%.

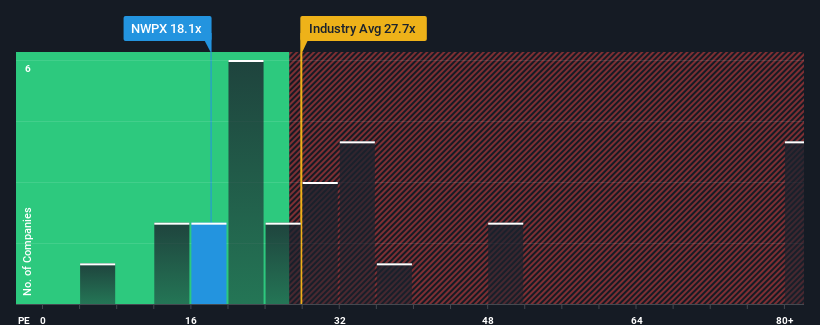

Despite the significant price increase, there are not many who consider Northwest Pipe’s price-to-earnings (P/E) ratio of 18.1 to be worth mentioning, as the median P/E in the U.S. is similar at around 18. However, it is not wise to simply ignore the P/E ratio without explanation, as investors may miss a special opportunity or a costly mistake.

Northwest Pipe has struggled recently as its earnings have declined faster than most other companies. One possibility is that the P/E ratio is modest because investors believe the company’s earnings trajectory will eventually fall in line with most other companies in the market. If you still like the company, you’ll want to see a turnaround in earnings trajectory before making any decisions. If not, existing shareholders may be a little nervous about the viability of the share price.

Check out our latest analysis for Northwest Pipe

Do you want the full picture of analyst estimates for the company? Then our free The Northwest Pipe report will help you find out what’s on the horizon.

Is there growth for Northwest Pipe?

Northwest Pipe’s P/E ratio would be typical for a company expected to deliver only moderate growth and, importantly, performance in line with the market.

Looking back, last year saw the company post a frustrating 9.5% drop in earnings. Despite this, earnings per share are up 48% year-on-year overall, regardless of the last 12 months. So, first of all, we can say that the company has done a very good job of growing its earnings overall during this time, even if there have been some hiccups along the way.

According to the three analysts who cover the company, earnings per share are expected to grow 4.5% annually over the next three years, well below the 10% annual growth forecast for the overall market.

With that in mind, it’s odd that Northwest Pipe’s P/E ratio is in line with most other companies. It seems that most investors ignore the fairly limited growth expectations and are willing to pay more to own the stock. These shareholders could be setting themselves up for future disappointment if the P/E ratio falls to a level more in line with the growth prospects.

The last word

Shares have risen significantly, and Northwest Pipe’s P/E ratio is now back to the market median. Generally, we prefer to use the price-to-earnings ratio only to determine what the market thinks about the overall health of a company.

We found that Northwest Pipe is currently trading at a higher than expected P/E ratio because its forecast growth is lower than the overall market. When we see a weak earnings forecast with slower than market growth, we suspect the share price could decline, driving the modest P/E ratio lower. This puts shareholders’ investments at risk and potential investors risk paying an unnecessary premium.

The company’s balance sheet is another important area for risk analysis. Take a look at our free Balance sheet analysis for Northwest Pipe with six easy checks of some of these key factors.

Naturally, If you take a closer look at some good candidates, you may come across a fantastic investment. So take a look at the free List of companies with a strong growth track record and a low P/E ratio.

Valuation is complex, but we are here to simplify it.

Discover if Northwest Pipe could be undervalued or overvalued with our detailed analysis, with Fair value estimates, potential risks, dividends, insider trading and the company’s financial condition.

Access to free analyses

Do you have feedback on this article? Are you concerned about the content? Contact us directly from us. Alternatively, send an email to editorial-team (at) simplywallst.com.

This Simply Wall St article is of a general nature. We comment solely on the basis of historical data and analyst forecasts, using an unbiased methodology. Our articles do not constitute financial advice. It is not a recommendation to buy or sell any stock and does not take into account your objectives or financial situation. Our goal is to provide you with long-term analysis based on fundamental data. Note that our analysis may not take into account the latest price-sensitive company announcements or qualitative materials. Simply Wall St does not hold any of the stocks mentioned.